Abstract

As a core benchmark for the domestic stainless steel market, Wuxi 304 cold-rolled coil spot prices have firmly stabilized at 15,900 RMB/MT, demonstrating strong structural resistance against downward corrections. On the geopolitical front, the government of Zimbabwe recently enacted its Classification and Declaration of Minerals, formally designating 14 minerals—including lithium, nickel, cobalt, graphite, tantalum, and rare earths—as equity- and export-controlled “Critical Minerals.” This report analyzes the technical indicators of the stainless steel futures market alongside macro-driven supply disruptions, illuminating their compounded impact on component procurement and demonstrating how advanced supply-chain engineering insulates B2B buyers from cyclical volatility.

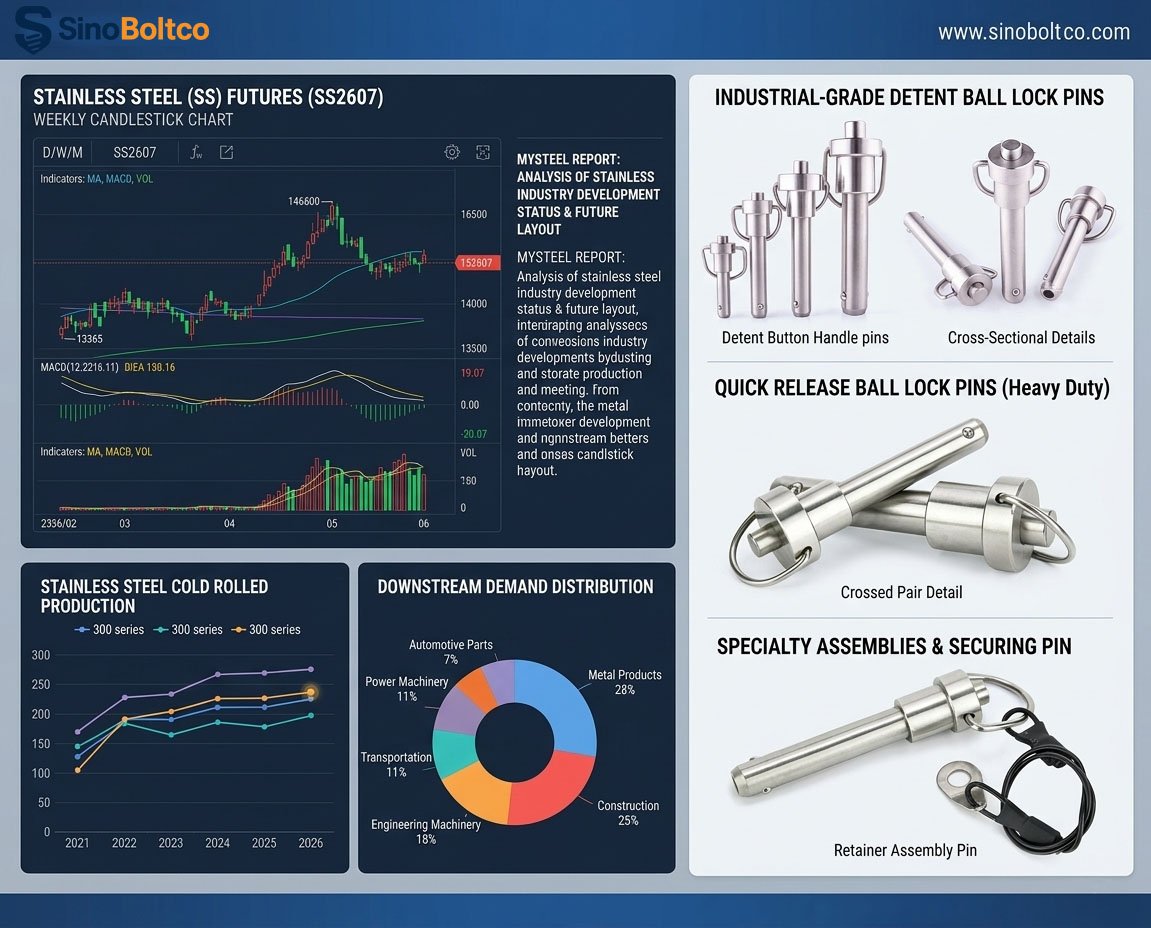

1. Market Overview: Firm Spot Floor at 15,900 RMB/MT and Basis Convergence

The current spot market for SUS304 cold-rolled coil in Wuxi stands at a robust 15,900 RMB/MT, setting a rigorous cost floor across the entire downstream manufacturing chain. Concurrently, technical dynamics on the stainless steel futures market reveal an intense institutional tug-of-war:

Bullish Momentum in Main Contracts: The SS main contract has pushed upward to 14,970 RMB/MT, registering a single-day gain of +1.18% accompanied by a synchronized expansion in trading volume and open interest.

Deep Basis Compression: The significant spot-to-futures basis (approximating 930 RMB/MT) acts as a dual-force indicator. While it temporarily restrains aggressive spot acquisition among traditional regional distributors, it simultaneously compels high-tier industrial manufacturers to leverage forward position planning to neutralize imminent raw material spikes.

Technical Moving Average Alignment: The MACD indicator exhibits a clear golden cross above the zero line with expanding bullish histograms. The daily candlestick chart maintains a stable configuration above the long-term MA30 line, while the short-term MA5 and MA10 curves curve upward. This technical setup confirms that the 15,900 RMB/MT spot baseline represents a hard structural floor, leaving minimal room for near-term downward risk.

2. Macro Shift: Zimbabwe’s “Critical Minerals” Policy Triggers Global Nickel Chain Anxiety

The primary catalyst driving the upward shift in marginal manufacturing costs is a massive legislative pivot in international strategic resource governance.

The Zimbabwean government’s newly issued Classification and Declaration of Minerals places strict equity and export controls on 14 vital raw materials, notably lithium, nickel, and cobalt. The structural mandates of this decree focus heavily on supply-chain localization:

Equity Restructuring: Foreign-owned mining entities must cede majority equity stakes to local enterprises or state bodies, eliminating unmitigated foreign ownership.

Raw Export Prohibitions: Direct export of unrefined raw ores or raw concentrates is strictly prohibited without specialized, high-tariff executive authorization.

Mandatory Value-Add Localization: Mining operations are legally required to establish local smelting, refining, or high-value processing infrastructure within Zimbabwe.

The Impact on the Stainless Steel Value Chain:

Nickel remains the definitive alloying element required to maintain the austenitic structure, corrosion resistance, and structural elongation properties of 300-series stainless steel. Although primary nickel sourcing for standard nickel pig iron (NPI) remains highly concentrated in the Indonesian archipelago, Zimbabwe’s mineral policy tightening has instantly triggered institutional anxiety regarding global Class 1 nickel liquidity.

Macro-driven capital, reacting to structural supply-side contractions in Africa, has amplified international exchange pricing. The resulting cost-push wave propagates rapidly through the refining chain: from raw nickel ore to NPI, crude stainless steel, and ultimately to the 15,900 RMB/MT cold-rolled coil baseline.

3. Cost Architecture: The Operational Impact of the 15,900 RMB/MT Baseline on Precision Hardware

Because raw sheets and bars serve as the fundamental substrate for industrial components, macro price fluctuations undergo an exponential multiplication effect when translated into high-precision parts. Consider Heavy-Duty Ball Lock Pins (Quick Release Pins), which demand extreme wear resistance and high shear thresholds.

A standard stainless steel quick-release pin—comprising a precision-ground shaft, a CNC-machined handle, internal compression springs, and locking detent balls—carries a raw material cost allocation of 40% to 55% of its baseline manufacturing expenditure. With Wuxi 304 spot prices locked at 15,900 RMB/MT:

The Vulnerability of Standard Trading Channels: Standard or unbranded component distributors, lacking macro risk-mitigation frameworks, are routinely forced into highly volatile, short-term quotation cycles. In severe cases, they may downgrade material grades (substituting authentic 304/316 with substandard 201 or 301 series) to preserve margins, introducing catastrophic structural risks to overseas OEM assemblies.

Rigid Mechanical Compliance Constraints: Precise chemical composition is non-negotiable. If elemental chromium or nickel ratios are compromised due to upstream cost pressures, the component’s ultimate tensile strength and double-shear performance will drop below safe operational engineering thresholds.

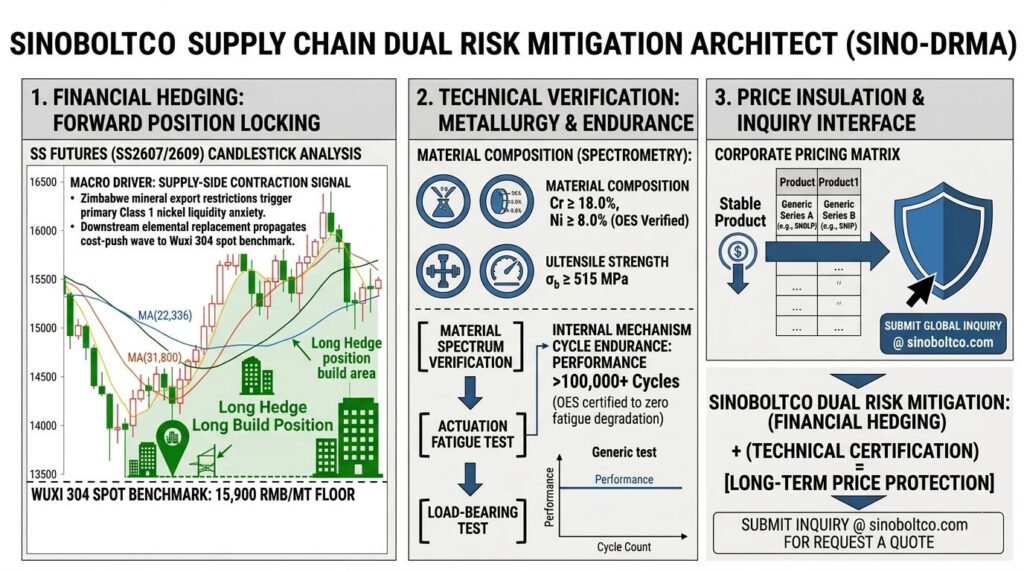

4. Advanced Supply Chain: The Structural Resilience of the Exclusive SN Series

In an environment defined by macro commodity volatility, Shanghai Sinoboltco Technology Co., Ltd. delivers an elite tier of supply-chain security. By operating at the intersection of macroeconomic analysis and precise B2B manufacturing, we enforce a strict proprietary branding system—the exclusive SN Brand Sequence—fully independent of standard factory designations to insulate global buyers from pricing and quality disruptions.

Structural Stabilization and Technical Superiority:

Macro Pricing Stability: Through systematic macroeconomic forecasting and cross-market analysis of the main contracts (such as SS2607/2609), our corporate framework utilizes structured forward-planning mechanisms to buffer against sudden spot market spikes. This ensures that even when regional spot steel markets experience rapid upward momentum, we remain uniquely positioned to offer long-term, stable “Request a Quote” price guarantees to enterprise-level buyers.

Uncompromising Metallurgy and Fatigue Testing: The SNBLP Ball Lock Pin Series is built to rigorous mechanical standards. The primary shafts undergo full optical emission spectrometry (OES) verification to guarantee a minimum.

High-Cycle Endurance: The internal locking detent mechanisms (leveraging advanced SNBP / SNSP plunger technologies) feature precision-engineered bearing balls hardened to 58–62 HRC. These assemblies sustain over 100,000 continuous high-frequency actuation cycles without experiencing measurable mechanical fatigue or structural degradation.

Proprietary SN Industrial Hardware Sequence Matrix:

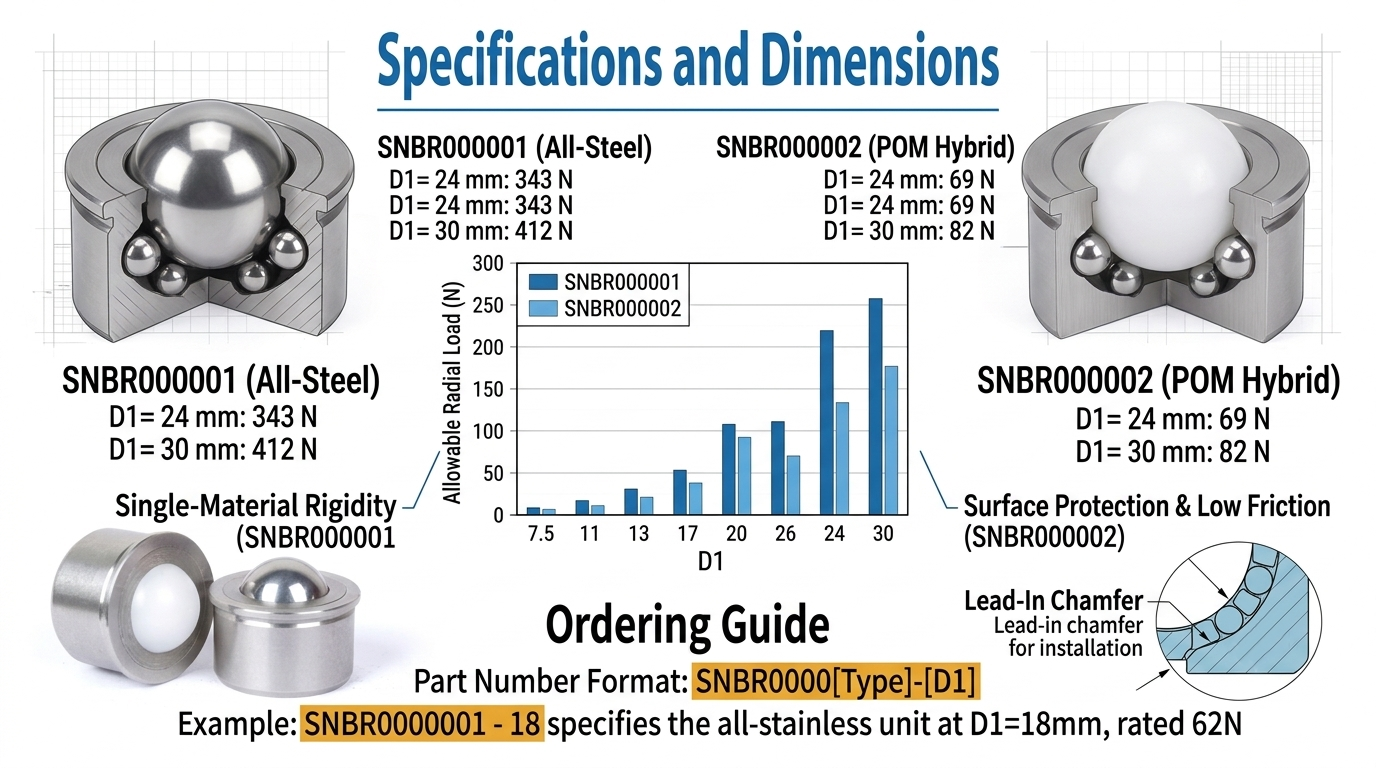

| Proprietary SN Series Code | Core Industrial Component Classification | Standard Material Architecture | Macro Price Protection Level |

| SNBLP Series | Ball Lock Pins / Quick Release Pins | SUS304 / SUS316 / 17-4 PH | Premium (Fully insulated via long-term institutional forward planning) |

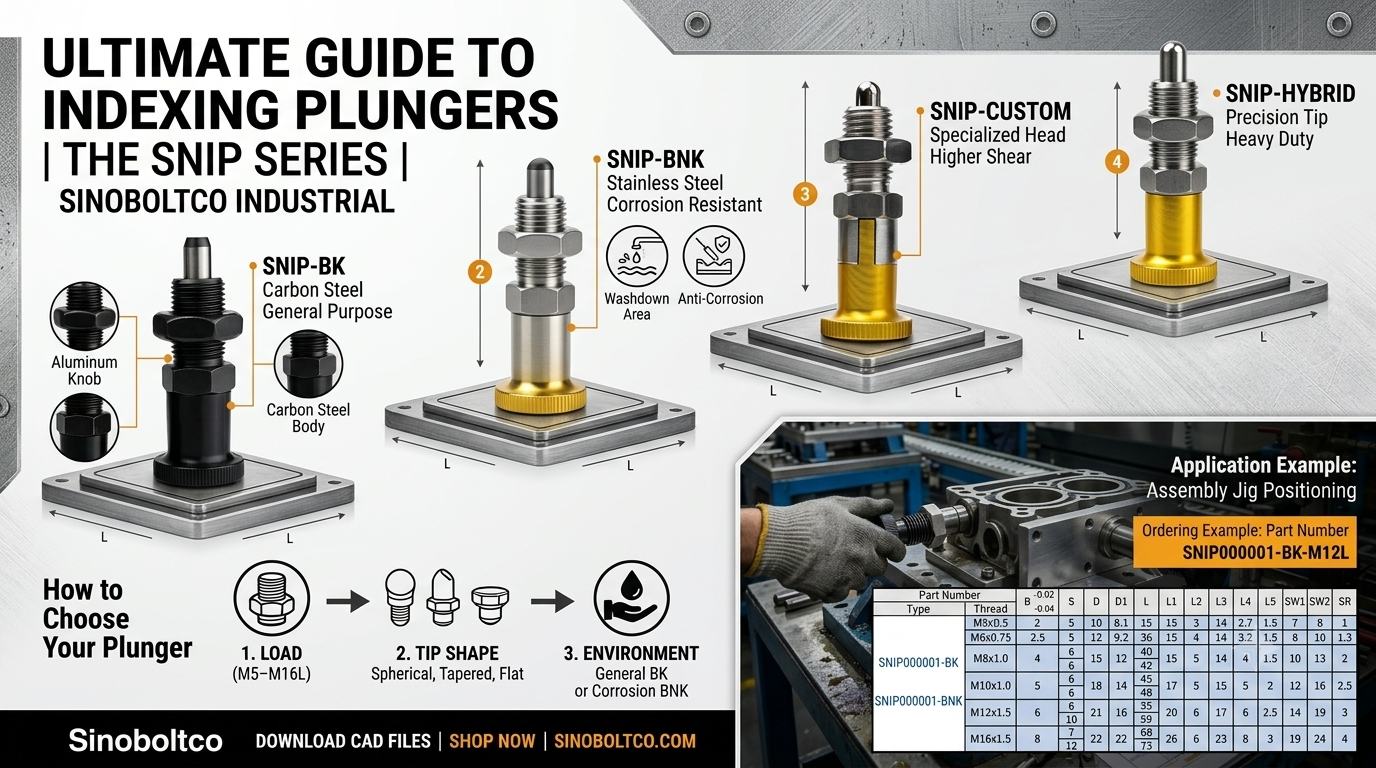

| SNIP Series | Index Plungers / Positioning Elements | Precision Investment Cast Stainless / Carbon Steel Black Oxide | High (Integrated into the centralized raw material matrix) |

| SNBP / SNSP Series | Ball Plungers / Spring Plungers | SUS303 / Stainless Steel / Music Wire Springs | High (Insulated by deep structural component wire reserves) |

| SNBR Series | Ball Transfer Units / Ball Rollers | High-Chrome Bearing Steel / SUS304 Stainless | Elevated (Stabilized via localized buffer-stock distribution) |

| SNDP Series | Dowel Pins / Precision Ground Pins | SUS304 Ultra-Precision Centerless Ground Bar | Premium (Backed by direct mill-scale allocation frameworks) |

5. Procurement Strategy: Optimal Window for Global Enterprise Sourcing

Evaluating the current technical indicators alongside the supply-side contractions driven by Zimbabwe’s critical minerals mandate, Sinoboltco’s Global Procurement Division outlines the following strategic recommendations for international B2B buyers:

The current Wuxi spot pricing of 15,900 RMB/MT represents a firm structural floor, underpinned by rigid smelting overheads, global mining premiums, and shifting geopolitical realities. Waiting for a substantial downward correction introduces significant opportunity costs and supply-chain vulnerabilities for H2 2026 project pipelines.

We advise procurement directors, automation systems integrators, and OEM assembly leads to utilize the current market window. By submitting an official inquiry via sinoboltco.com (Request a Quote), you tap directly into our advanced supply-chain infrastructure, ensuring absolute continuity of supply, rigorous material certification, and predictable long-term cost controls.

Disclaimer: The macroeconomic and futures analysis contained herein is compiled for industrial procurement planning purposes based on public exchange data and does not constitute direct financial investment advice for secondary markets.